The Financing Process

How do home loans actually work?

The home loan process can feel overwhelming at first. By collaborating with a trusted lender and staying informed through every step, from pre-approval to closing, you can have a significantly more comfortable experience. We recommend consulting with a mortgage specialist to find a professional who will provide you with the best guidance and care.

To get an idea of what to expect, review the following home loan process steps.

Step One:

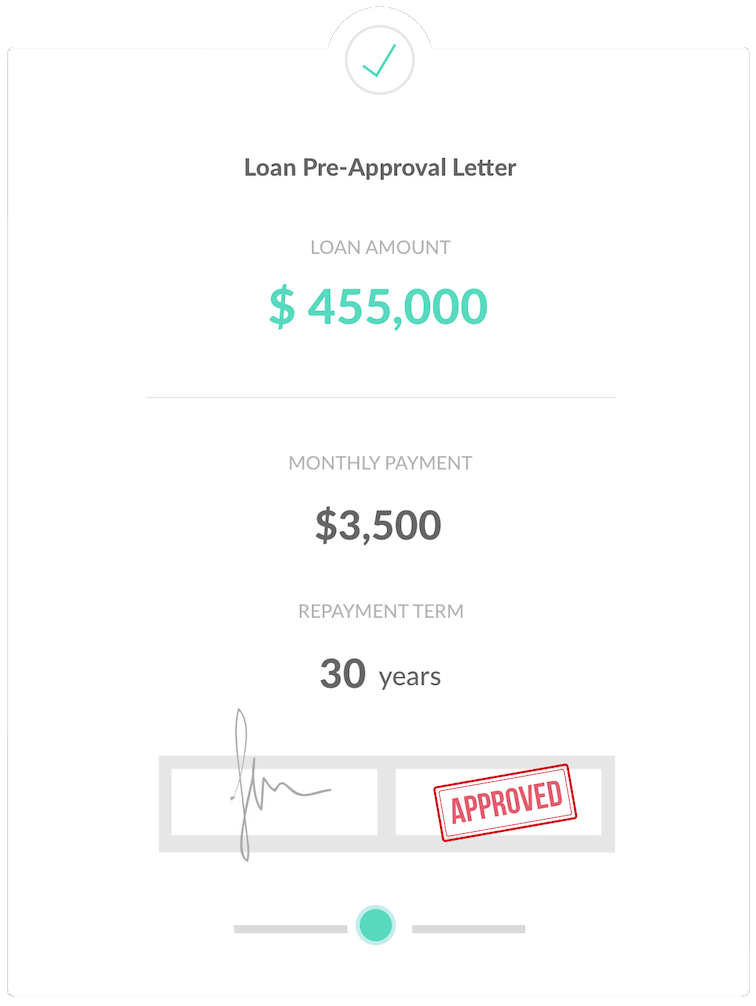

Get Pre-Approval

Before you start looking for a home to buy, it’s wise and proactive to meet with a lender to get pre-approved for a loan amount. Offers accompanied by a pre-approval letter are stronger and will stand out, especially when the seller is receiving multiple offers.

To gain pre-approval, your preferred lender will gather information about income, assets, and debts to help determine how much you can borrow. This includes gathering a credit report, W-2 forms, pay stubs, federal tax returns, and recent bank statements.

There are a variety of home loan programs offering different advantages depending on your unique needs and preferences. Your preferred lender can go over the specifics of each to ensure you find a loan option that best aligns with your needs.

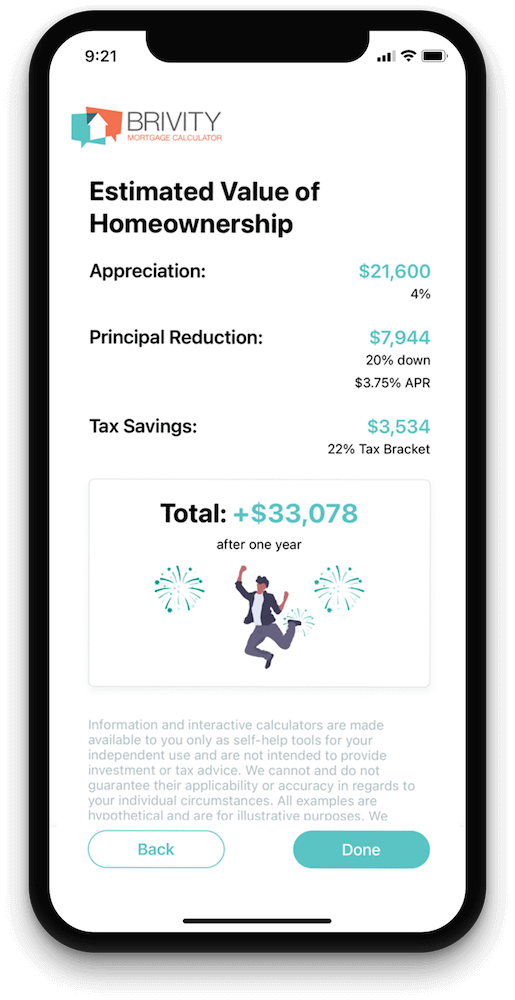

Estimate Your Monthly Payment

Estimate your mortgage payment, including the principal and interest, taxes, insurance, HOA, and Private Mortgage Insurance.

Price

Annual Tax

Loan Term (Years)

Down Payment %

Interest Rate %

Monthly HOA

Monthly Insurance

$3,198.20

Estimated Monthly Payment

Principal

$2,398.20

(75.0%)Taxes

$500.00

(15.6%)Private Mortgage Insurance (PMI)

$0.00

(0.0%)HOA

$100.00

(3.1%)Insurance

$200.00

(6.3%)

Step Two:

Find the best loan

Collaborating with a top-notch local loan officer will ensure you have access to competitive rates and programs that best fit your individual needs. Take the first step by completing this form to get connected today!

Step Three:

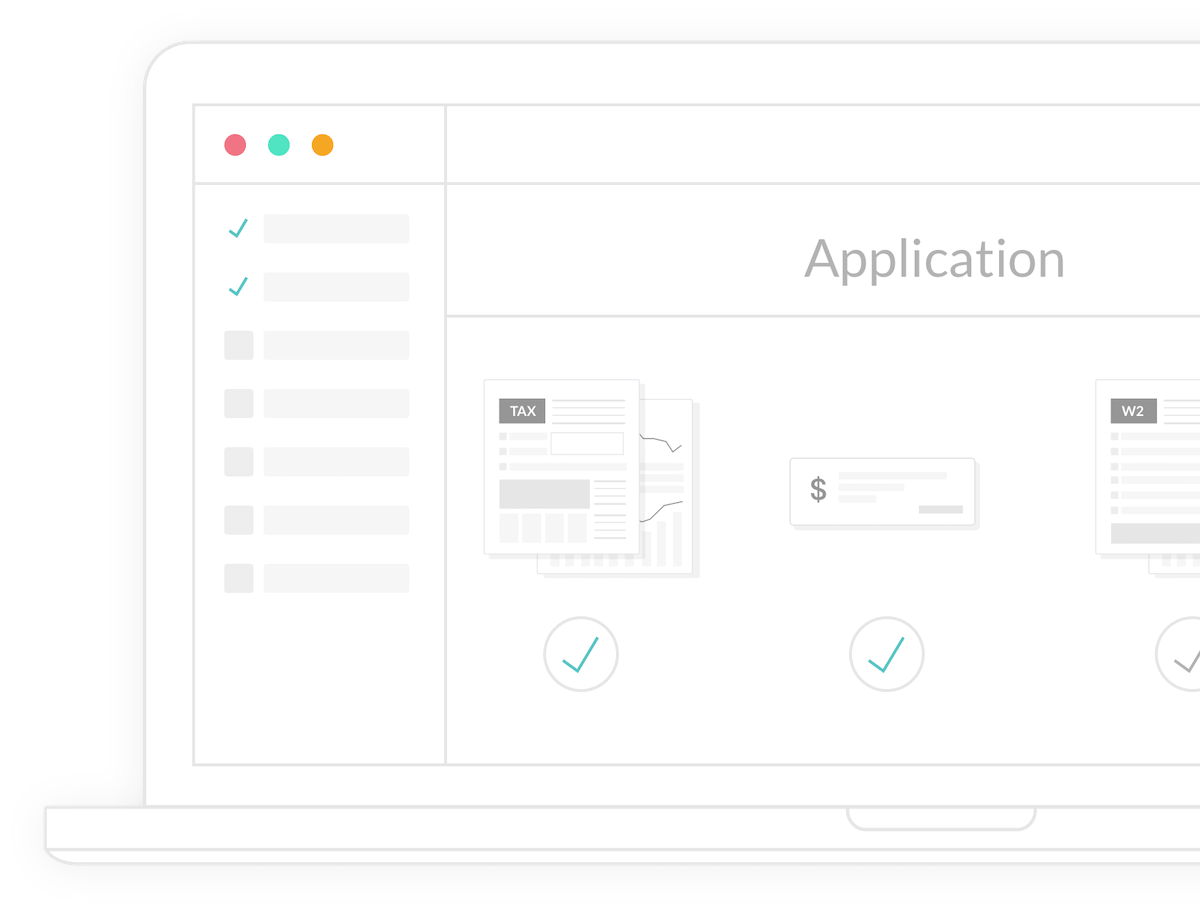

Application and processing

When you find the perfect property and your offer is accepted, your lender will help you complete a full mortgage loan application, discuss down payment options, and explain any related fees.

Then, your application is submitted for processing where the documents are reviewed. Your lender will also order a home appraisal and a property title search.

The next part of the application process involves sending everything to an underwriter who will review and approve the entire loan package to make sure it meets all compliance regulations.

It is not unusual to receive requests for additional documentation or clarification during this phase of the application process.

Step Four:

Signing and finalizing the deal

Once your loan is approved, you'll need to set up homeowners insurance.

Your documents will be sent to the title company and the closing will be scheduled for you to sign the necessary paperwork and pay any additional costs to complete the purchase of your new home.

After the loan goes through the required recording process, the purchase is complete, and you officially own your new home!

Have Questions About Home Financing?

What is the difference between pre-qualification and pre-approval?

Pre-qualification is an informal estimate of how much you may be able to borrow based on self-reported financial information. Pre-approval is a more thorough process where a lender verifies your income, assets, and credit to issue a formal commitment. In competitive markets like New York, a pre-approval letter carries significantly more weight with sellers.

How much should I save for a down payment?

Down payment requirements vary by loan type. Conventional loans typically require 5% to 20%, while FHA loans may allow as little as 3.5%. Some programs for qualifying buyers offer even lower options. Your lender will help you identify the best fit for your financial situation and long-term goals.

Are there first-time homebuyer programs available in New York?

Yes. New York offers several programs designed to assist first-time buyers, including down payment assistance grants, reduced interest rate programs, and tax credit incentives. Eligibility varies by income, location, and property type. We can connect you with lenders who specialize in these programs to maximize your benefits.

What are closing costs and how much should I expect to pay?

Closing costs are fees associated with finalizing your mortgage and transferring ownership of the property. In New York, buyers should typically budget between 2% and 5% of the purchase price. These costs may include attorney fees, title insurance, recording taxes, and lender fees. Team Paley and your lender will provide a detailed estimate early in the process so there are no surprises.

How long does the mortgage approval process take?

The mortgage approval process typically takes 30 to 45 days from the time a full application is submitted. Timelines can vary depending on the complexity of your financial profile and the responsiveness of all parties involved. Staying organized and providing requested documentation promptly helps keep the process on track.